Why Tanzania’s export increase must now translate into a stronger external balance

Tanzania’s external sector position has undergone significant shifts over the past decade, with the latest quarterly data showing a notable narrowing of the current account deficit despite persistent trade imbalances.

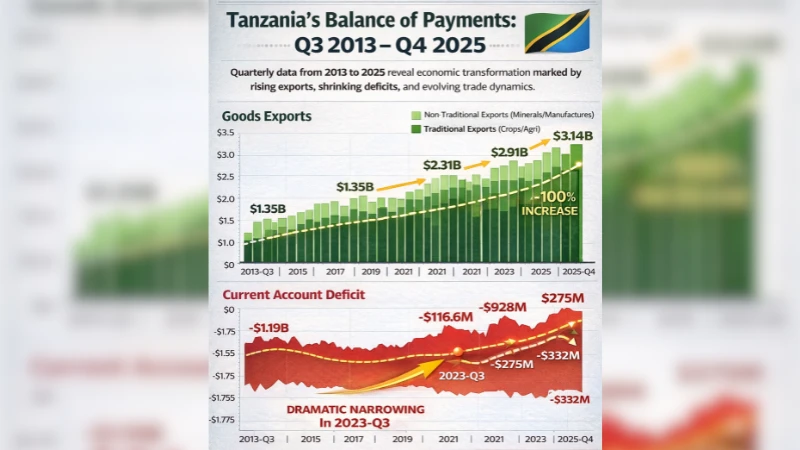

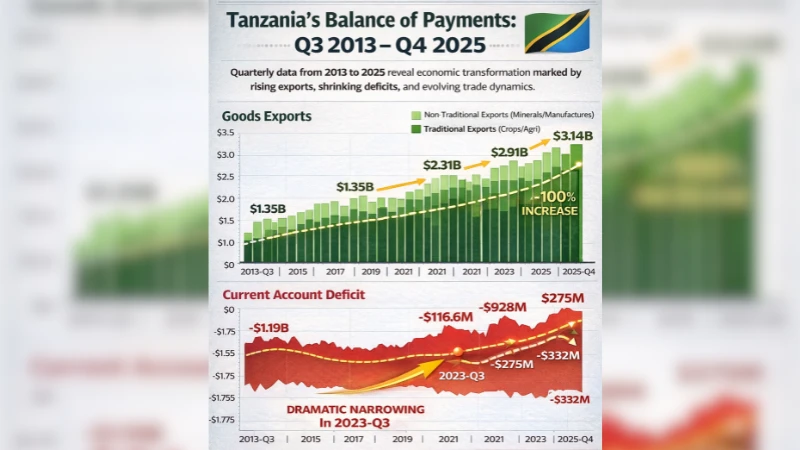

Quarterly figures from the Bank of Tanzania (BoT) tracking the country’s Balance of Payments from the third quarter of 2013 through the fourth quarter of 2025 reveal a dynamic trajectory shaped by export growth, import pressures, and evolving commodity trends.

In 2013 and 2014, Tanzania’s current account deficit remained wide, frequently exceeding $1 billion per quarter. For example, in 2014-Q1 the deficit stood at approximately $1.64 billion, reflecting strong import demand and relatively modest export earnings at the time.

Between 2015 and 2019, the deficit showed signs of gradual moderation, although it remained structurally negative. Quarterly gaps typically ranged between $500 million and $1.1 billion.

This period coincided with infrastructure expansion, rising capital goods imports and fluctuating global commodity prices, particularly for gold and agricultural exports.

A sharp turning point is visible in the 2023 data. In 2023-Q3, the deficit narrowed dramatically to around $116.6 million, marking one of the lowest quarterly shortfalls in over a decade. While the following quarter (2023-Q4) saw the deficit widen again to roughly $928 million, the overall trend suggests improved resilience in the external sector compared to earlier years.

By 2024 and into 2025, the deficit remained volatile but generally smaller than the multi-billion-dollar gaps seen in the mid-2010s.

In 2025-Q3 and 2025-Q4, the current account deficit stood at approximately $275 million and $332 million respectively — levels that, while still negative, represent a substantial structural improvement from the peaks of the past decade.

A key driver behind the improved external position has been a sustained rise in export earnings. Goods exports (f.o.b.) have more than doubled over the review period.

In 2013-Q3, goods exports were about $1.35 billion. By 2023-Q3, they had climbed to roughly $2.31 billion, and in 2024-Q4 exports reached approximately $2.91 billion. The upward momentum continued into 2025, with exports peaking at over $3.14 billion in 2025-Q4 — the highest quarterly figure in the dataset.

The composition of exports also reveals important structural shifts. Traditional exports — including crops such as coffee, cotton and cashew nuts — were relatively modest in the early years, often below $200 million per quarter. However, there were notable spikes, including about $831 million in 2024-Q4 and $839 million in 2025-Q4, suggesting stronger agricultural performance and possibly improved global prices or volumes.

Non-traditional exports, which include minerals, manufactured goods and other diversified products, have shown particularly strong growth.

From under $1 billion in many quarters between 2013 and 2015, non-traditional exports rose steadily to surpass $1.8 billion in 2023-Q3 and exceeded $2.4 billion in 2025-Q3. This growth underscores Tanzania’s ongoing diversification efforts and the rising importance of mining and value-added sectors.

Despite the export gains, the current account remains in deficit largely because of sustained import demand. Tanzania’s development strategy — anchored in infrastructure, industrialisation and energy investment — has required significant capital goods imports.

While detailed import figures are embedded within the broader current account components, the persistent negative balance indicates that import growth has often kept pace with or exceeded export expansion, particularly during large-scale infrastructure phases.

However, the narrowing of the deficit in recent quarters suggests a more favourable balance between export receipts and import payments. Stronger commodity earnings, increased gold exports, and possibly improved services receipts such as tourism have likely contributed to this adjustment.

The data span several global and domestic shocks, including commodity price swings, global financial volatility and the Covid-19 pandemic period. Although the pandemic years are not explicitly broken out in the summary rows provided, the moderate deficits in the early 2020s compared to the mid-2010s suggest that Tanzania’s external accounts proved more resilient than in previous cycles.

The sharp narrowing in 2023-Q3 stands out as a potential structural shift, indicating that export capacity may be catching up with import-intensive growth. That said, the subsequent widening in 2023-Q4 and fluctuations through 2024 and 2025 highlight ongoing vulnerability to external shocks and seasonal trade patterns.

The strong export performance in 2024 and 2025, culminating in record quarterly goods exports above $3 billion, signals improved external competitiveness. The rising contribution of non-traditional exports suggests that Tanzania’s diversification strategy is gaining traction.

However, the persistence of quarterly deficits — even if smaller — indicates that the economy remains dependent on imported capital goods, fuel and intermediate inputs. Sustaining the narrowing trend will likely depend on continued export diversification, enhanced value addition in agriculture and mining, and stable global demand conditions.

If the momentum seen in 2025 is maintained, Tanzania could move closer to a structurally balanced current account over the medium term. But given the volatility observed across quarters, policymakers will need to manage external risks carefully, particularly in an environment of uncertain global commodity prices and tightening international financial conditions.

Overall, the decade-long data depict a country gradually strengthening its external earnings capacity while still navigating the realities of an import-dependent growth model. The trajectory is encouraging, but consolidation remains a work in progress.

Top Headlines

Trending Stories

© 2026 IPPMEDIA.COM. ALL RIGHTS RESERVED