BoT: Private sector lending accelerates money supply to 62.5trn/- in December

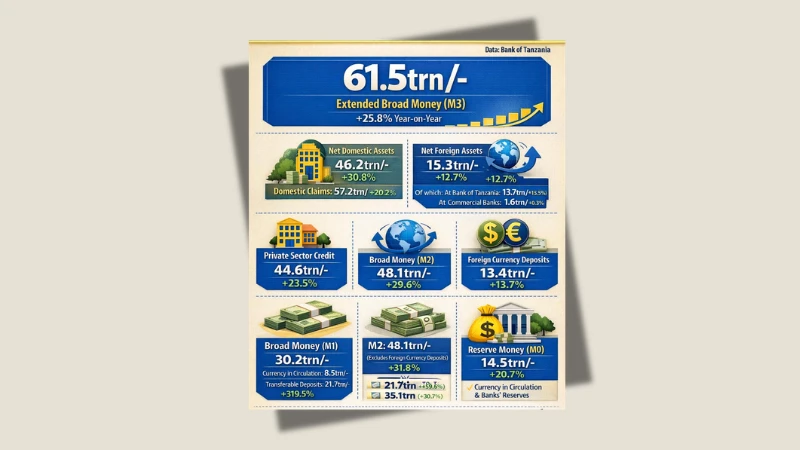

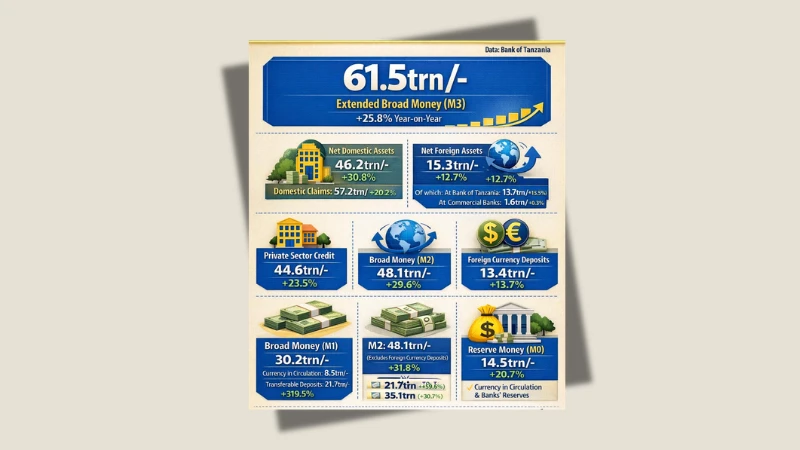

Tanzania’s money supply maintained a strong upward trajectory in December 2025, with extended broad money (M3) rising to 61.5trn/-, reflecting robust private sector credit growth and sustained liquidity in the banking system, according to the latest figures from the Bank of Tanzania (BoT).

On an annual basis, M3 expanded by 25.8 per cent, accelerating from 22.9 per cent recorded in November and more than double the 11.1 per cent growth posted in December 2024, when money supply stood at 48.9trn/-.

The data signal an increasingly accommodative monetary environment aligned with the country’s strong economic growth momentum.

The expansion was primarily driven by net domestic assets, which climbed by 30.8 per cent year-on-year to 46.2trn/-. Domestic claims, the largest component of net domestic assets, increased by 20.2 per cent to 57.2trn/-.

Credit to the private sector remained the central engine of monetary growth. Lending to businesses and households rose by 23.5 per cent to 44.6trn/-, up from 36.1trn/- in December 2024.

The acceleration from 18.1 per cent in November indicates strengthening demand for financing across key sectors of the economy, including trade, agriculture, mining, transport and construction.

Banks’ holdings of government securities also increased by 18.7 per cent to 9.6trn/-, demonstrating that financial institutions continue to balance credit expansion with investments in relatively low-risk Treasury instruments.

Broad money (M2), which excludes foreign currency deposits, grew by 29.6 per cent to 48.1trn/-, underscoring strong growth in shilling liquidity.

Narrow money (M1) expanded by 31.8 per cent to 30.2trn/-, largely driven by a 39.6 per cent surge in transferable deposits to 21.7trn/-. Currency in circulation rose by 15.5 per cent to 8.5trn/-.

Foreign currency deposits increased at a more moderate pace of 13.7 per cent to 13.4trn/-, suggesting relatively contained dollarisation pressures. Meanwhile, net foreign assets of the banking system stood at 15.3trn/-, marking a 12.7 per cent annual increase.

Reserve money (M0) rose by 20.7 per cent to 14.5trn/-, reflecting accommodative liquidity management.

From a macroeconomic perspective, the strong expansion in money supply reflects deepening financial intermediation and growing confidence in the domestic economy.

The acceleration in private sector credit indicates that banks are increasingly channeling funds toward productive sectors, supporting investment, working capital financing and consumption activities.

The sharp rise in transferable deposits is particularly significant. It points to increased use of formal banking channels for transactions, likely supported by expanding digital payment systems and greater financial inclusion.

This structural shift enhances monetary policy transmission and improves the efficiency of the financial system.

However, the pace of monetary growth warrants careful monitoring. While inflation remains within the official 3–5 per cent target range, sustained growth of M3 above 25 per cent could, if not matched by corresponding increases in output, create future price pressures.

The current environment suggests that liquidity expansion is broadly aligned with economic activity, but policy authorities will need to ensure that credit growth continues to support productive investment rather than speculative or consumption-driven excesses.

Encouragingly, the relatively moderate growth in foreign currency deposits signals stable confidence in the local currency, reducing risks associated with external vulnerability.

At the same time, continued growth in net domestic assets underscores the economy’s reliance on internal drivers rather than external flows.

Overall, the December 2025 monetary data portray a banking sector operating with strong liquidity buffers and expanding credit to the real economy.

If managed prudently, the current trend positions Tanzania to sustain growth momentum into 2026 while maintaining macroeconomic stability.

Top Headlines

Trending Stories

© 2026 IPPMEDIA.COM. ALL RIGHTS RESERVED