Capitalisation rates key to benchmark property market, academic study finds

Property capitalisation rates remain central to valuing real estate assets and benchmarking market performance, with implicit valuation models often offering greater robustness than explicit discounted cash flow (DCF) approaches, according to an education briefing published in the Journal of Property Investment & Finance.

In the briefing, Denis Camilleri of Dhi Periti, Floriana, Malta, examines how capitalisation rates are constructed and how they capture market expectations of growth.

He argues that in less transparent markets, such as Malta’s, implicit valuation models based on market-derived capitalisation rates may provide more reliable estimates of market value than explicit DCF models, which rely heavily on forecast assumptions.

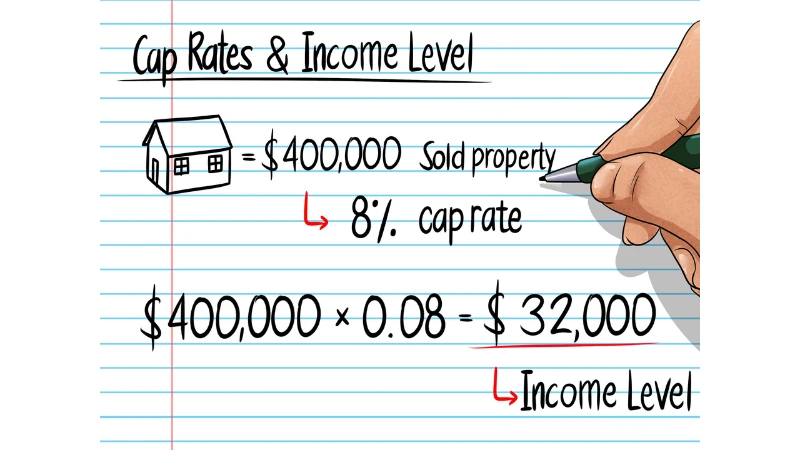

A capitalisation rate is used to convert annual rental income into an estimate of capital value. Because growth expectations are embedded within the rate itself, it is described as an implicit valuation model.

By contrast, a DCF model explicitly projects rental income, capital growth and cash flows over a defined period—typically 10 years in property valuation—and discounts them back to present value.

The briefing suggests that while explicit DCF models can be useful in the short term, they should be applied sparingly for long-term valuations. Instead, market-derived capitalisation rates may better reflect long-run growth expectations and risk, particularly in commercial property sectors such as offices, retail outlets and trading properties including hotels and schools.

Capitalisation rates can be derived from observed initial yields in the market—calculated as net rental income divided by capital value—or built up using reference models where transactional evidence is limited.

Camilleri highlights Gordon’s growth model as a framework for understanding how capitalisation rates relate to broader capital market variables.

Under Gordon’s model, the initial yield reflects the risk-free rate of return, premiums for liquidity and tenant risk, expected rental growth and depreciation.

The formula illustrates the close relationship between property markets and capital markets, particularly the influence of the risk-free rate, often proxied by government bond yields.

One of the model’s strengths, the author argues, is that it produces an implied average annual growth rate over the life of the investment. If this average growth rate is applied consistently within a DCF model, both implicit and explicit approaches should theoretically yield the same valuation outcome.

However, he cautions that explicit models can introduce bias. In buoyant markets, valuers may be tempted to apply higher short-term growth rates, potentially inflating valuations.

Given the unpredictability of economic shocks—such as the 2008 global financial crisis, the Covid-19 pandemic in 2019 and the geopolitical and inflationary pressures following the Russia–Ukraine war—forecasting precise growth patterns over a 10-year horizon can be highly uncertain.

An analysis of Malta’s capital and property markets supports the argument for stability in property yields. Data from the Central Bank of Malta show significant volatility in government bond yields over time, particularly in shorter maturities. By contrast, property initial yields have demonstrated relatively limited variation.

For example, the initial yield adopted for an office block in Floriana declined gradually from 7 percent in 1988 to around 4.75–4.85 percent between 2018 and 2020, a variation of just over two percentage points across more than three decades. During the same period, DCF discount rates fell from 14 percent in 1988 to around 6.25–6.75 percent in recent years.

The relationship between the DCF discount rate and the capitalisation rate reflects implied growth expectations, expressed simply as capitalisation rate equals target rate minus growth. By deducting the initial yield from the discount rate, valuers can estimate the market’s implied growth expectation for a given year.

The relatively low volatility of property yields compared to stock market performance further reinforces the perception of property as a hedge against inflation. According to the briefing, Malta’s stock exchange has exhibited significantly greater fluctuations than the residential property market over the same period.

Camilleri concludes that valuation methods must reflect the transparency and mechanics of the local market.

In Malta, where transactional data may be limited, the implicit capitalisation approach—anchored in market rents and observable yields—can provide a more stable and defensible framework.

Ultimately, the study underscores the importance of professional judgement. Valuers must understand both property and capital markets, and be able to determine and justify an appropriate market capitalisation rate, taking into account risk, growth expectations and the level of market transparency.

As financial markets evolve and global shocks continue to test forecasting models, the briefing argues that grounding property valuations in market-derived capitalisation rates may offer a more resilient benchmark for assessing long-term value.

Top Headlines

Trending Stories

© 2026 IPPMEDIA.COM. ALL RIGHTS RESERVED